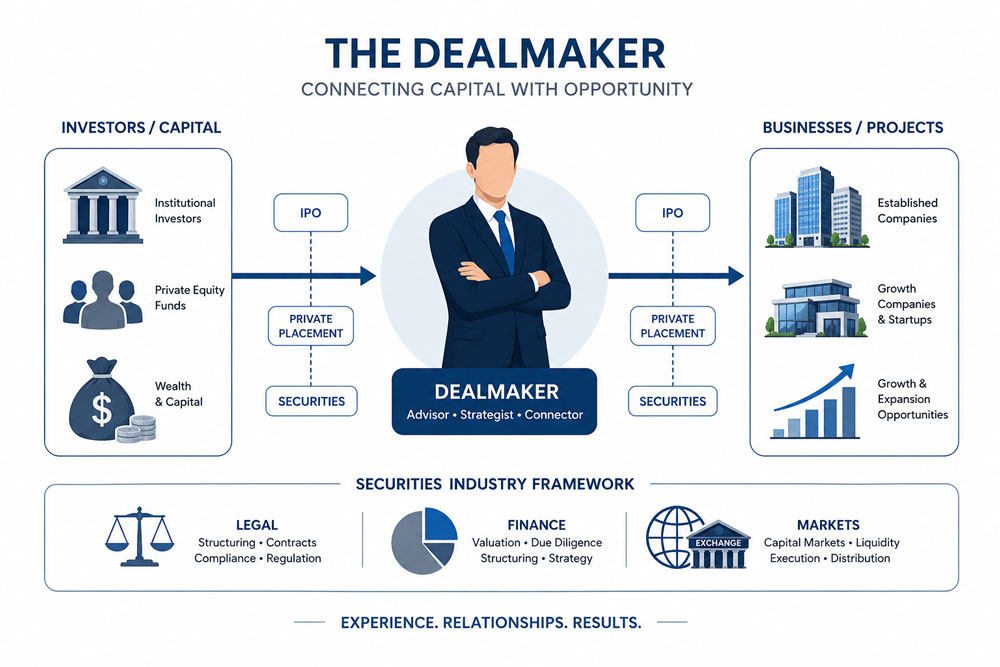

In the securities industry, the “Dealmaker” is best understood as a function, not a single legal title. In formal U.S. broker-dealer taxonomy, the closest role is the investment banking representative: Financial Industry Regulatory Authority says the Series 79 registration covers advising on or facilitating debt and equity offerings, mergers and acquisitions, tender offers, restructurings, asset sales, divestitures, and business combination transactions, while the Series 82 registration is tailored to soliciting and selling private placement securities in primary offerings. In practice, however, the same commercial function also appears inside issuer treasury teams, corporate-development groups, private credit and private equity firms, and capital-markets legal and accounting workstreams. The Dealmaker’s actual job is to convert a commercial objective into a priced, documented, executable, and closable transaction.

The core of the role is orchestration. A strong Dealmaker finds the opportunity, screens counterparties and investors, runs due diligence, turns risk into structure, converts structure into documentation, manages approvals and market communication, and then gets the transaction over the line and into the post-close operating or monitoring phase. The most authoritative sources across markets all point to this same reality: SEC forms and tender-offer rules make disclosure and timing central in the U.S.; FCA sponsor guidance makes due care, skepticism, and third-party challenge central in the U.K.; and ESMA’s prospectus, market-abuse, securitization, and product-governance materials make structured process, inside-information discipline, and investor-protection design central in the EU.

The hardest legal fault line is often not economics but licensing. A Dealmaker who is not FINRA licensed is not automatically in breach; the risk depends on what the person actually does. The risk becomes acute when an unregistered person solicits investors, materially participates in securities negotiations, or takes transaction-based compensation for effecting securities transactions for others. FINRA Rule 2040, the statutory broker definition, and SEC enforcement actions such as the Ranieri matter show why firms care: even sophisticated private-fund fundraising can cross into unregistered broker activity, bringing penalties, bars, supervisory consequences, and expensive re-papering of mandates and compensation structures.

Jurisdiction now matters more than ever. The regulatory center of gravity differs across the United States, the European Union, and the United Kingdom. The UK’s new public-offers-and-admissions regime took effect on January 19, 2026; much of the EU Listing Act framework applies from June 5, 2026; and U.S. M&A timetables have been affected by the modernized HSR filing regime that took effect in February 2025. At the same time, ESMA’s 2026 AI work and the FCA’s AI Lab show that technology is moving from peripheral support to a core deal-execution issue, especially in diligence, surveillance, and communications recordkeeping.

What the Dealmaker Is

A good Dealmaker combines five roles that are often spread across an institutional chart but must be integrated in the transaction itself. First, the Dealmaker is an originator who identifies a financing need or strategic opening. Second, the Dealmaker is an analyst who converts imperfect information into valuation, structure, and downside cases. Third, the Dealmaker is a translator who turns business objectives into legal terms, disclosure, and investor messaging. Fourth, the Dealmaker is a quarterback who coordinates bankers, traders, lawyers, auditors, sponsors, boards, and regulators. Fifth, the Dealmaker is a closer who gets signatures, approvals, settlement mechanics, and post-close accountability aligned at the same moment. FINRA’s Series 79 scope, the FCA’s sponsor due-diligence note, and SEC and PCAOB materials all reinforce that the role is inherently cross-functional rather than purely sales-oriented.

That is why “Dealmaker” cuts across job titles. In a bank or broker-dealer, it may sit in industry coverage, M&A, equity capital markets, debt capital markets, leveraged finance, structured finance, or private placements. In an issuer, it may sit in treasury, finance, or corporate development. In a fund or sponsor, it may sit in capital formation, portfolio finance, or deal execution. In law and accounting, the function appears as issue-spotting, diligence leadership, verification, comfort, and transaction architecture. The market does not reward narrow brilliance nearly as much as it rewards the ability to connect valuation, legal constraints, and human incentives under deadline.

The skills profile is therefore broader than textbook finance. Technical fluency matters, but so do pattern recognition, process discipline, investor psychology, drafting judgment, skepticism, and the ability to separate negotiable points from existential ones. FCA guidance is explicit that sponsors should show curiosity and a skeptical mindset, challenge assumptions, test sensitivities, and decide when independent evidence is needed rather than relying solely on management representations. That is an unusually direct regulatory statement of what elite dealmaking already looks like in practice.

Career paths usually start with analytical apprenticeship and move toward judgment and client ownership. FINRA’s exam structure reflects this progression: Series 79 emphasizes data collection, underwriting and new-financing transaction types, and M&A and restructuring work; Series 82 emphasizes business development, account opening, recommendation and recordkeeping, and processing private-placement transactions. The difference is telling. Junior Dealmakers first learn how a transaction works; senior Dealmakers learn which transaction should exist at all, when it should be launched, and how to keep it alive when conditions deteriorate.

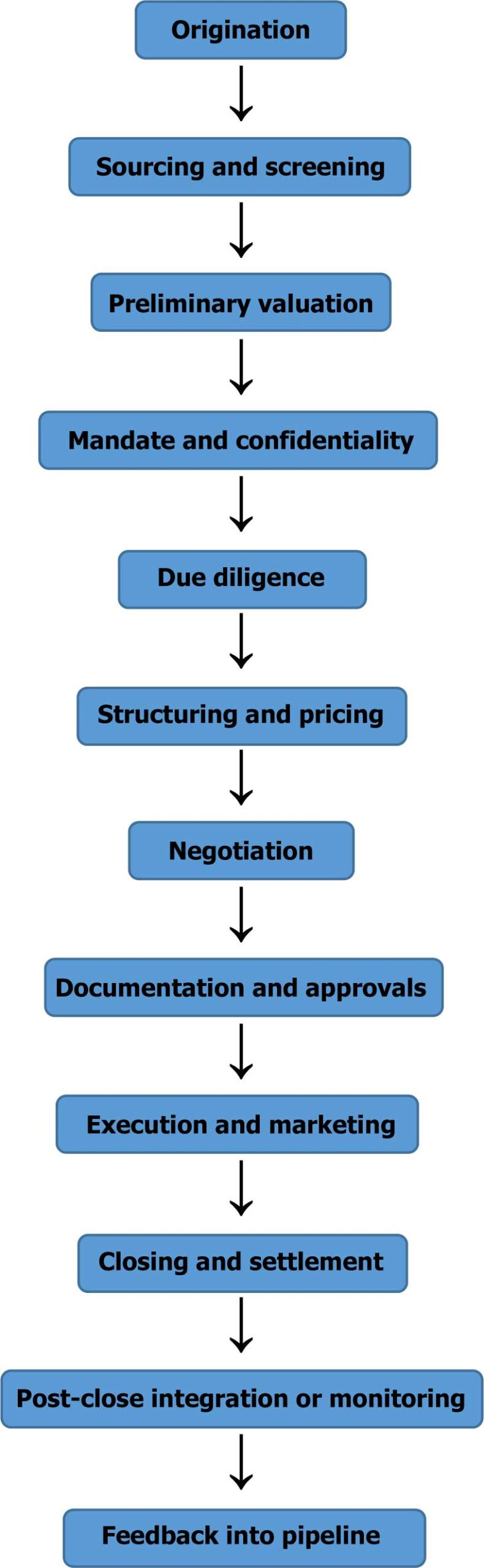

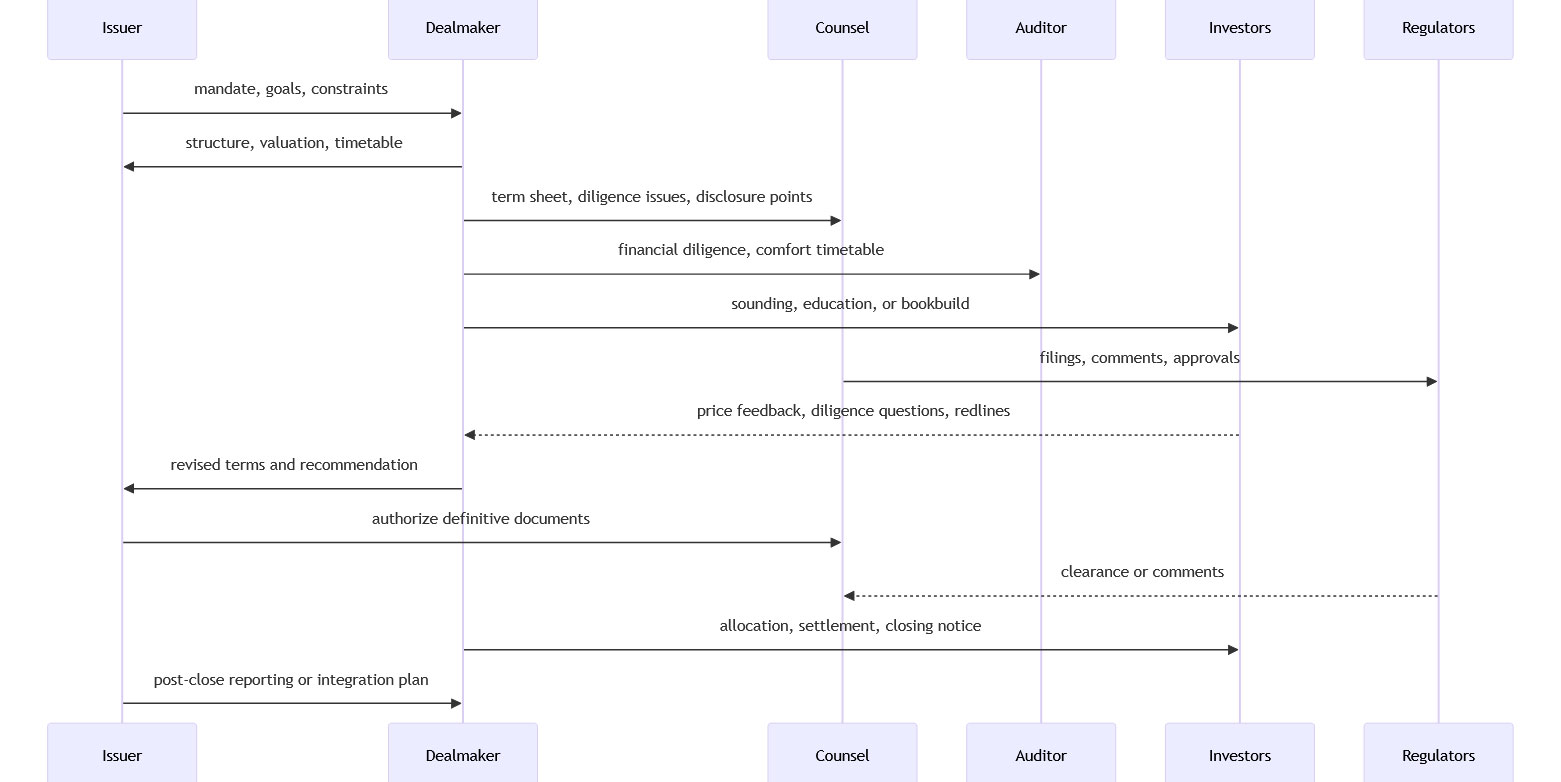

How Deals Move from Idea to Closing

The deal lifecycle is best seen as a controlled reduction of uncertainty. At origination, uncertainty is strategic: should this company raise equity, issue debt, sell assets, acquire a target, do a PIPE, or defer? At sourcing, uncertainty is counterparty-specific: which investors, buyers, or financing channels are live? At due diligence, uncertainty becomes factual: what is true, what is missing, and what can change the valuation or legal exposure? At structuring, uncertainty becomes economic and regulatory: what combination of instrument, covenant, disclosure, approval, and timetable can survive both market scrutiny and rulebook constraints? At negotiation and documentation, uncertainty becomes textual: which risks are shifted, shared, capped, or disclosed? At execution and closing, uncertainty becomes operational: are approvals, comments, conditions, funds flow, settlement, and public communications aligned? And after closing, uncertainty becomes managerial: did the economics work, and are servicing, integration, reporting, or monitoring doing what the underwriting case assumed?

This lifecycle is a synthesis of the process architecture embedded in SEC offering and M&A forms, FCA sponsor due-diligence guidance, PIPE documentation conventions, and ABS disclosure and reporting rules.

A useful way to think about the stages is not merely sequentially but diagnostically. Origination tests thesis quality. Sourcing tests market access. Due diligence tests truthfulness and completeness. Structuring tests ingenuity under rule constraints. Negotiation tests relative leverage and discipline. Documentation tests precision. Execution tests timing and communication. Closing tests operating control. Post-close monitoring tests whether the original underwriting story was actually robust. Each phase solves a different problem, which is why strong dealmakers change posture as the transaction advances: expansive and curious early, skeptical and comparative in the middle, exact and procedural near signing and close.

| Stage | Core question | Typical outputs | Dominant skills | Common failure mode |

|---|---|---|---|---|

| Origination | Why this deal now? | thesis, mandate, target investor/buyer universe | pattern recognition, sector judgment | pursuing a market window without a real need |

| Sourcing | Who can actually transact? | pipeline, shortlist, soundings, NDAs | networking, market intelligence, qualification | confusing interest with executable demand |

| Due diligence | What is true, and what matters? | diligence reports, issue lists, QA logs | skepticism, legal/financial literacy | relying on management assurances alone |

| Structuring | How should risk and value be allocated? | term sheet, valuation range, covenant package, instrument design | financial modeling, regulatory fluency | optimizing one variable while breaking another |

| Negotiation | Which points determine economics or certainty? | revised terms, markups, board materials | prioritization, empathy, firmness | spending leverage on low-value items |

| Documentation | Can the deal survive disclosure and enforcement review? | purchase agreement, underwriting agreement, prospectus, circular | drafting judgment, verification, process control | ambiguity, inconsistency, weak bring-downs |

| Execution and closing | Can we price, allocate, settle, and disclose cleanly? | order book, allocations, approvals, funds flow, releases | timing, communication, crisis management | last-minute mismatch between docs, approvals, and settlement |

| Post-close | Did the original case hold? | integration plans, investor reporting, servicing, covenant monitoring | follow-through, analytics, governance | treating signing as the finish line |

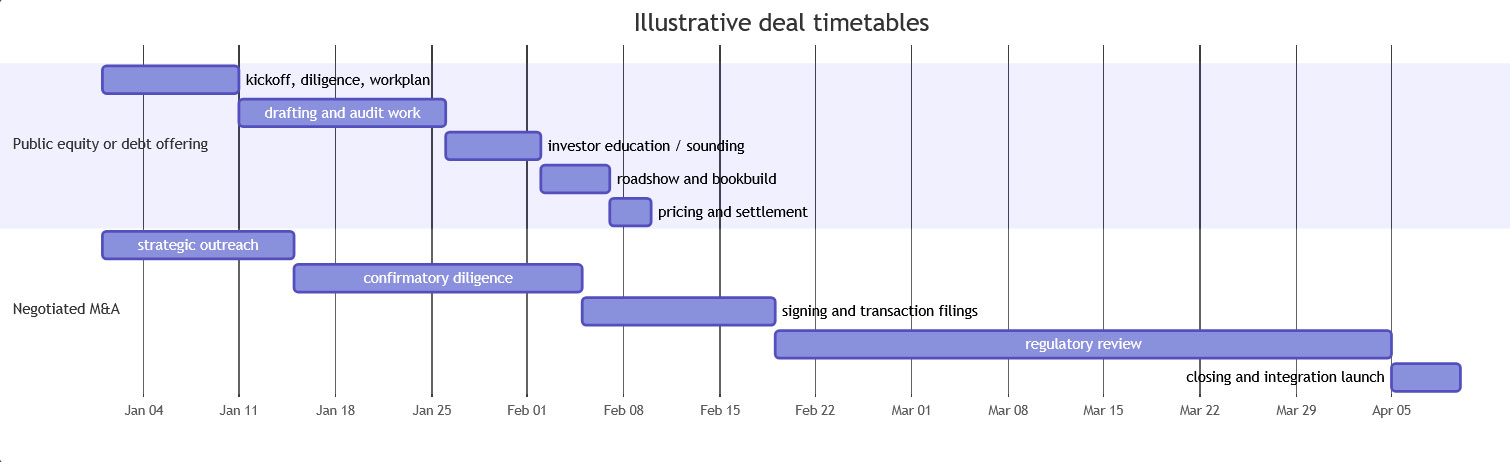

The durations above are illustrative rather than prescriptive. Actual timing varies by issuer readiness, audit status, jurisdiction, and antitrust or sector approvals. What is fixed in the U.S. is that tender offers must remain open for at least 20 business days, and qualifying M&A transactions may not close until any required HSR waiting period has expired or been terminated.

Deal Types and Analytical Toolkit

A securities Dealmaker commonly works across seven recurring transaction families: registered equity offerings, debt issuances, M&A, exempt private placements, PIPEs, securitizations, and structured products. These are not interchangeable. A registered equity deal solves for market access and disclosure credibility. A debt deal solves for cost of capital, tenor, covenant flexibility, and ratings or investor classes. M&A solves for control, synergies, and strategic positioning. Private placements solve for speed, confidentiality, and targeted capital. PIPEs solve for urgency and execution certainty in public-company capital raising, often at a cost in discount and governance complexity. Securitizations solve for balance-sheet efficiency and asset-specific funding. Structured products solve for engineered payoff exposure and investor targeting, while creating special disclosure and product-governance burdens.

| Deal type | Primary objective | Typical core documents | Main pricing variables | Central Dealmaker challenge |

|---|---|---|---|---|

| Registered equity offering | raise common or preferred capital in the public market | registration statement, prospectus, underwriting agreement, 8-K or exchange announcements | discount to market, size, allocation quality, aftermarket support | balancing valuation, dilution, and execution certainty |

| Debt issuance | raise term funding at acceptable spread and covenant package | shelf or offering memorandum, indenture, underwriting or purchase agreement | coupon/spread, tenor, ranking, covenants, ratings | matching investor demand to leverage and flexibility |

| M&A | transfer control or combine businesses | merger agreement, proxy/prospectus on Form S-4, tender-offer materials, financing commitments | purchase price, premium, form of consideration, reverse break fee, conditions | optimizing value without losing certainty of close |

| Private placement | raise exempt capital quickly and selectively | PPM or OM, subscription docs, side letters, Form D in the U.S. | valuation or discount, governance rights, transfer restrictions | finding the right investors without public-market process |

| PIPE | inject capital into a public company on a private basis | purchase agreement, registration-rights agreement, resale registration mechanics | discount, reset or anti-dilution terms, warrant coverage, resale path | speed versus dilution and market overhang |

| Securitization | fund or de-risk asset pools | prospectus or OM, pooling and servicing, sale docs, trust docs, reports | asset performance, enhancement, tranche thickness, retention | making legal structure, data, and collateral analytics line up |

| Structured products | manufacture tailored market exposure | base prospectus, supplements, pricing supplement, risk factors, product-governance files | payoff formula, barriers, issuer credit, fees, hedging cost | explaining complexity and ensuring target-market suitability |

Source synthesis: SEC exempt-offering materials, Rule 144A and Regulation S materials, SEC PIPE guidance, Form S-4 and tender-offer guidance, SEC ABS rules, and ESMA/FCA structured-product materials.

On valuation, the Dealmaker almost never relies on a single model. The standard toolkit triangulates intrinsic value, current market value, transaction value, and downside liquidity value. Academic valuation literature and leading market-practice frameworks still converge on the same three broad pillars: discounted cash flow, relative valuation through market multiples, and option-style valuation where payoffs are nonlinear. In M&A, precedent transactions remain important because they capture control premiums and market-clearing prices; in financings, trading comparables and debt-capacity analysis often matter more than a theoretically pristine DCF. In convertibles, structured products, and some preferred or warrant financing, option logic stops being optional and becomes central.

The practical model stack usually includes an operating model, a DCF, trading comparables, precedent transactions, sensitivity analysis, and at least one “deal-consequence” model tailored to the situation: accretion/dilution for public-company M&A, debt-capacity or refinancing models for leveraged deals, waterfall models for securitization, and scenario trees for rescue capital or PIPEs. FCA sponsor guidance is especially useful here because it makes explicit what sophisticated teams already know: forecast preparation, historical forecasting accuracy, model assumptions, sensitivities, and downside cases are not appendices to a model; they are the real work.

Tax and accounting can change a strong-looking deal into a bad one. Under IFRS 3, business combinations use the acquisition method and focus on fair value of consideration, acquired assets and liabilities, and resulting goodwill or bargain purchase gains. IAS 32 then becomes critical where the instrument sits on the debt-equity boundary, because classification depends on whether the issuer has a contractual obligation to deliver cash or another financial asset. On the tax side, the IRS’s OID rules matter because discount on debt instruments is generally taxed as interest over the life of the instrument, and the tax-free reorganization rules under Section 368 can determine whether a stock-heavy M&A structure preserves tax efficiency. The Dealmaker therefore has to understand not just headline value, but also how value travels through earnings, leverage ratios, distributable reserves, covenants, and after-tax proceeds.

Public offerings also carry a distinct liability architecture. Section 11 of the Securities Act creates civil liability for material misstatements or omissions in a registration statement, and auditor comfort letters exist partly because underwriters and other parties with a due-diligence defense need third-party assurance around financial information. This is why financial modeling in a real deal is never a free-standing spreadsheet exercise. It is entangled with disclosure controls, document verification, accountant procedures, and legal judgment.

Law, Regulation, and Ethics

The regulatory baseline differs materially across the U.S., EU, and UK, and outside those jurisdictions this report does not specify local law. Within scope, however, the central pattern is clear: each regime tries to solve the same problems of disclosure, market abuse, investor protection, and orderly execution, but with different legal plumbing and timing consequences.

In the U.S., the first organizing question is whether the offering is registered or exempt. Registered financings generally run through SEC forms such as S-1, S-3, F-1, or F-3, while business combinations involving securities consideration commonly use Form S-4 and cash tender offers use Schedule TO. Exempt transactions typically rely on Regulation D, Rule 144A, and/or Regulation S. For public offerings involving FINRA members, Rule 5110 requires review of underwriting terms and arrangements unless an exemption applies. Layered on top are anti-fraud and market-conduct rules, including Section 11 and Section 12 liability, Regulation M’s anti-manipulation restrictions during distributions, and Regulation FD’s selective-disclosure discipline.

In the EU, the key pillars are the Prospectus Regulation, MAR, MiFID II product-governance requirements, and the Securitisation Regulation. Prospectus obligations turn on whether securities are publicly offered or admitted to trading, MAR governs inside information, insider lists, and market soundings, MiFID II product governance requires manufacturers and distributors to identify target markets and distribution strategies, and the securitization rulebook overlays due diligence, transparency, and risk-retention obligations. The EU Listing Act, published in late 2024, is intended to simplify access to public markets, with much of the regime applying from June 5, 2026. ESMA’s 2026 consultations on delayed disclosure under MAR show that deal timing and communications practice in Europe are still evolving in material ways.

In the U.K., the regime has diverged further after Brexit. The FCA’s new Public Offers and Admissions to Trading Regulations framework and the Prospectus Rules: Admissions to Trading on a Regulated Market sourcebook took effect on January 19, 2026. For certain equity listings, the sponsor regime remains central: the FCA explicitly characterizes sponsors as guide-and-assurance providers, expects due care and careful enquiry, and makes clear that responsibility cannot simply be delegated to outside experts. For market abuse, the U.K. retains a MAR-based architecture, including market-sounding practice. For M&A control, parties must also consider the U.K. merger regime administered by the CMA, and in public takeovers the U.K. Takeover Code remains a critical overlay.

| Topic | US | EU | U.K. | Deal impact |

|---|---|---|---|---|

| Public-offer architecture | SEC registration and liability framework | Prospectus Regulation | FCA PRM / POATRs from Jan. 19, 2026 | disclosure drafting and clearance timing differ materially |

| Inside information and market sounding | anti-fraud, Reg FD, Reg M, tender-offer rules | MAR and ESMA guidelines | UK MAR and FCA rules | communication scripts and wall-crossing controls must be jurisdiction-specific |

| Private placements | Reg D, Rule 144A, Regulation S | exemptions under Prospectus Regulation plus local law | private / non-public routes under U.K. regime, depending on facts | distribution planning is a legal design problem, not a sales afterthought |

| M&A approval layer | S-4 / Schedule TO plus HSR if applicable | EU Merger Regulation if thresholds met | CMA merger review and Takeover Code where applicable | certainty of close can dominate nominal price |

| Structured products and securitization | SEC disclosure focus, Reg AB, FINRA communications | MiFID II product governance, MAR, Securitisation Regulation | FCA PROD and U.K. securitization / conduct rules | product design and investor targeting are as important as pricing |

Source synthesis: SEC, FINRA, ESMA, FCA, FTC, European Commission, and CMA materials.

When the Dealmaker Is Not FINRA Licensed

This is the issue that most often converts a commercial win into a regulatory problem. The broker definition focuses on a person engaged in the business of effecting transactions in securities for the account of others. FINRA’s 2025 modernization notice also points to the main functional indicators courts consider: solicitation, involvement in negotiations between issuer and investor, and transaction-related compensation. As a practical inference from that framework, an internal issuer or acquirer employee generally presents less broker-registration risk than an outside consultant or finder, because the internal employee is acting for the principal rather than for the account of others. But once a person outside the issuer is soliciting investors or buyers, shaping the securities terms, and taking a success fee, the risk rises sharply.

The licensing consequence is concrete. FINRA’s own materials say representative-level qualification exams require association with and sponsorship by a FINRA member or other SRO member firm. Series 79 is the principal investment-banking registration and covers advisory and facilitation work on offerings and M&A; Series 82 is narrower and covers solicitation and sale of private placement securities. Series 79 itself draws an important line: preparing or advising on a marketing plan can fall within Series 79, but active road-show selling and direct investor interactions generally trigger Series 7 or Series 82 requirements depending on the offering type. There is, in other words, no “freelance capital-raising license” untethered from a regulated firm.

FINRA Rule 2040 makes the economic implication severe: a member generally may not pay transaction-based compensation to an unregistered person if doing so would require the person to be registered as a broker-dealer under Section 15(a). FINRA and the SEC also continue to treat transaction-based compensation as a powerful indicator of broker status, even if it is not absolutely determinative by itself. That means firms cannot “paper over” a risky compensation structure simply by calling the person a consultant, strategic adviser, or rainmaker. Function beats label.

There is a narrow but important carveout in the M&A context. The SEC’s 2014 M&A Brokers no-action position, later withdrawn after Congress enacted a statutory exemption, recognized that a limited class of brokers could effect securities transactions in connection with the transfer of ownership and control of privately held operating companies without broker-dealer registration, subject to conditions. The conditions included no public offering, no shell company other than certain business-combination shells, no custody of funds or securities, and a buyer that would actively operate the business. Congress’s statutory exemption added size and revenue limitations. This relief is useful, but it is not a general capital-raising exemption and it does not solve ordinary private-placement or PIPE fundraising.

| Scenario | Broker / FINRA risk | Why | Practical mitigation |

|---|---|---|---|

| Internal treasury or corp-dev lead at the issuer or buyer | lower, but not zero | acting for the principal rather than effecting transactions for others | document role, keep regulated selling under the broker-dealer or dealer-manager where needed |

| Unregistered consultant on a fixed advisory retainer | medium | title does not control; conduct still matters | confine work to analysis, project management, and internal strategy |

| Unregistered consultant on a success fee | high | transaction-based compensation is a major broker-status indicator | move mandate to a registered placement agent or broker-dealer affiliate |

| Unregistered person soliciting investors or road-showing a private offering | very high | solicitation and sale of private placements are core Series 82 activities | require sponsored registration and supervised communications |

| M&A broker transferring control of a private operating company | potentially lower if exemption fits | statutory M&A broker carveout is narrow and conditional | test every condition before relying on it |

This table is a functional synthesis of the broker definition, FINRA Rule 2040, Series 79 and Series 82 scopes, and the M&A broker exemption pathway. It is not a substitute for legal advice on specific facts.

Ethics and compliance run far beyond licensing. Across jurisdictions, Dealmakers must control conflicts of interest, inside information, selective disclosure, recordkeeping, AML and sanctions exposure, anti-bribery risk, and communication quality. FCA AML guidance continues to emphasize risk-based systems and controls; DOJ and SEC FCPA guidance reminds transaction teams that cross-border expansion or state-linked counterparties can create bribery exposure; and U.S. anti-manipulation and disclosure rules remain active constraints throughout an offering or tender process. Ethical Dealmaking therefore means more than avoiding fraud: it means building a process where incentives, disclosures, scripts, clearances, and audit trails are designed to withstand later review.

Negotiation, Technology, and Economics

Negotiation in securities deals is not one negotiation. It is a stack of linked negotiations, each with a different audience and currency. The issuer or seller negotiates price and certainty with investors or buyers. Counsel negotiates drafting asymmetries and disclosure calibration. Bankers negotiate economics, allocation, timing, and market support. Auditors negotiate comfort scope and timing. Regulators negotiate none of these in the commercial sense, but they determine what is legally possible and when. Sophisticated practice materials on cross-border and takeover transactions repeatedly show that value is won less by aggression than by sequencing: knowing which issue to raise with which party, and when.

The most reliable tactics are therefore procedural rather than theatrical. Strong Dealmakers define reserve positions before the meeting, rank issues by value and certainty impact, avoid trading against themselves by over-explaining early, and maintain a single source of truth for term-balance changes across markups, board decks, and investor messages. They also know when not to negotiate: inside-information rules, prospectus liability, and core regulatory filings are not “commercial asks.” A team that treats disclosure or market-sounding rules as bargaining chips is usually signaling weak process, not strength.

This sequence reflects how offering, M&A, and sponsor processes are actually divided across institutions, as evidenced by SEC filing mechanics, FCA sponsor duties, and auditor comfort-letter practice.

Technology has become a first-order dealmaking variable. The modern stack typically includes virtual data rooms, relationship and pipeline systems, diligence automation, model and comparable-data tools, and compliance archives. Public vendor materials show why these categories matter: virtual data rooms such as Datasite position themselves around due diligence and transaction management; Intapp markets DealCloud around relationship and deal analysis; and AI contract-review providers such as Kira Systems and Luminance emphasize diligence-scale document analysis. None of these tools removes judgment. What they do is compress search, sort, issue-spotting, and workflow latency.

Regulators now treat AI as both an efficiency source and a control risk. ESMA’s 2026 work on AI adoption in securities markets is based on survey evidence and highlights benefits, use cases, and challenges from deployment. The FCA’s AI Lab and 2026 innovation work show a similar posture: encourage adoption, but only with safe and responsible implementation. FINRA, for its part, has already flagged the recordkeeping and supervision challenges created by AI-generated chatbots, meeting transcripts, and other digital communications. For dealmakers, that means AI can help summarize thousands of diligence documents or compare precedents, but it can also create discoverability, privilege, hallucination, and off-channel-record risk if governance lags adoption.

Compensation is powerful because it shapes behavior at every stage of the lifecycle. In broker-dealers and banks, junior dealmakers are usually paid salary plus bonus; senior dealmakers are paid on a mix of group results, individual fee credit, franchise value, and risk-adjusted deferred compensation. FINRA’s corporate-financing rules indirectly affect the economics of public offerings by reviewing underwriting compensation and terms. In prudentially regulated firms, remuneration rules also matter: the UK removed its banker bonus cap in 2023, and subsequent FCA and PRA reforms continued to reshape the balance between fixed and variable pay. The right conclusion is not that dealmakers are “overpaid” or “underpaid,” but that incentive design is itself a risk-management question. If the pay plan rewards volume over suitability, or announcement over close, the process will degrade even with excellent people.

| Compensation dimension | Typical structure | Main risk | Best-practice implication |

|---|---|---|---|

| Junior execution staff | salary plus discretionary bonus | optimizing for activity rather than judgment | tie bonus to quality, teamwork, and error avoidance |

| Mid-level deal leads | higher variable pay tied to execution and client development | pushing marginal deals to preserve pipeline optics | include close rates and risk-adjusted outcomes |

| Senior rainmakers and partners | highly variable compensation, often deferred and subject to governance limits in regulated firms | overemphasis on fee generation and underweighting of conduct | use deferral, clawback, and committee review |

| Underwriting and distribution teams | deal fees subject to fairness and regulatory review | hidden or unreasonable economics | maintain transparent allocation and filing discipline |

| Issuer-side treasury or corp-dev teams | salary, annual bonus, and sometimes equity | short-term deal metrics over long-term integration or servicing | include post-close performance measures |

A precise title-by-title pay table is difficult to support from official public data because labor datasets do not map cleanly onto securities-firm titles such as analyst, associate, vice president, director, and managing director. What can be said confidently is that compensation becomes more variable, deferred, and conduct-sensitive as seniority and regulatory accountability rise.

Case Studies and Best-Practice Playbooks

Arm Holdings plc

Arm’s 2023 IPO is a clean example of how a Dealmaker solves a cross-border public-equity problem by combining corporate structuring, U.S. disclosure, underwriting coordination, and market timing. The SEC filing shows that the offering was of ADSs representing Arm ordinary shares, and that all of the ADSs sold in the IPO were sold by an existing shareholder rather than by the company itself. Arm later announced pricing of 95.5 million ADSs at $51.00 each, with trading to begin the next day, and exchange materials described it as the largest IPO of 2023 at roughly $4.87 billion raised. The underwriting agreement also identifies a multi-bank syndicate structure. The deeper lesson is that an IPO Dealmaker is not merely “selling stock”; the job is to choose issuer form, security form, selling-shareholder mechanics, bookbuilding strategy, syndicate architecture, and public-market narrative at the same time.

Broadcom Inc. and VMware, Inc.

The Broadcom-VMware transaction illustrates that the hardest part of M&A dealmaking is often not headline price but duration, financing, and regulatory endurance. SEC filings show the parties signed a merger agreement in May 2022 and used a multi-step structure reflected in the proxy/prospectus materials. The SEC also noted that Broadcom filed an S-4 containing VMware’s proxy statement and a Broadcom prospectus, which the SEC declared effective in October 2022. On the antitrust side, the European Commission first opened an in-depth investigation and later cleared the transaction with commitments. Broadcom’s later debt offering materials then confirmed that acquisition financing had in fact been used to fund the VMware purchase and refinance related indebtedness. This is what complex dealmaking looks like in reality: not a single “M&A deal,” but a synchronized package of merger agreement, shareholder process, regulatory remedy, bridge and term financing, and post-signing risk management.

Ford Motor Credit Company LLC auto ABS program

Ford Credit’s auto ABS program shows why securitization changes the meaning of “closing.” SEC records for its 2024 owner and lease trusts show Rule 424(b)(2) prospectuses and related underwriting agreements filed in connection with note issuances, while monthly investor reports continue to disclose reserve levels, delinquency and extension data, and repurchase-demand activity after issuance. In other words, the Dealmaker in securitization has to think simultaneously like a capital-markets professional, a collateral analyst, a process lawyer, and a servicing-risk manager. The transaction is not finished when the notes are sold. It remains alive through data production, performance surveillance, and compliance reporting.

Ranieri Partners LLC

Ranieri is the clearest public illustration of the danger created by an unlicensed Dealmaker taking on broker-like fundraising functions. The SEC found that an outside consultant actively solicited investors for private funds managed by Ranieri affiliates and was paid approximately $2.4 million in transaction-based compensation. The SEC charged Section 15(a) violations; Ranieri and a former executive paid penalties, and the consultant was barred from the securities industry. This matters because the facts were not exotic: private funds, sophisticated investors, and a consultant embedded in capital raising. The case demonstrates that “sophisticated parties only” is not a defense to unregistered broker activity.

These four examples point to a common best-practice pattern. The Dealmaker succeeds when the commercial thesis, legal pathway, diligence architecture, communication discipline, and compensation arrangements are aligned before the market-facing phase starts. Failure usually occurs where one of those workstreams is treated as secondary.

A practical kickoff template should therefore answer six questions immediately: what objective the client is trying to achieve, why this path is better than the plausible alternatives, what the regulatory perimeter is, who the real decision makers are, what the downside case looks like, and who is authorized to speak externally. A diligence checklist should cover business, financial, legal, tax, regulatory, sanctions, cyber, data-room governance, and management-integrity items, with a clear issues list tied to valuation and disclosure rather than a generic document dump. A closing checklist should then map conditions precedent, approvals, comment clearance, bring-down diligence, signing and pricing authority, funds flow, settlement mechanics, and public communications in one place. FCA sponsor guidance, PCAOB comfort-letter practice, and SEC filing rules all support this “single control sheet” approach.

| Common pitfall | Why it happens | Mitigation |

|---|---|---|

| weak mandate definition | teams chase a financing format before defining the objective | force an alternatives memo at kickoff |

| diligence as document gathering rather than issue finding | pressure to move quickly | maintain a live red-flag register tied to valuation and disclosure |

| unlicensed finder economics | commercial teams want cheaper origination | centralize status review and ban contingent fees without registration analysis |

| model precision illusion | spreadsheets conceal fragile assumptions | run sensitivities, downside cases, and historical forecast checks |

| disclosure inconsistency | multiple drafts and audiences drift apart | maintain a single source of truth and verification ownership |

| regulatory sequencing errors | legal review starts too late | produce a jurisdictional approvals matrix before launch |

| treating close as the finish line | team incentives stop at announcement or settlement | tie performance to post-close integration, servicing, and covenant behavior |

This pitfalls table is grounded in SEC filing and liability mechanics, FCA sponsor expectations, post-close ABS reporting, and the Ranieri enforcement example.

Future Trends

The next decade of dealmaking will likely be shaped by four converging trends. The first is the continued expansion of private capital, especially private debt. Recent academic work from Harvard-affiliated researchers documents how private debt has become a major talent magnet relative to traditional banking. That matters because it changes where deal flow, structuring expertise, and relationship networks live. A Dealmaker increasingly needs to understand not just the public syndication window, but also direct lending, club structures, bespoke hold positions, and hybrid public-private pathways.

The second trend is regulatory modernization rather than simple deregulation. The UK’s new POATRs regime and the EU Listing Act are both intended to simplify capital formation, but they do so by redesigning disclosure architecture, not by abandoning investor protection. In M&A, the updated HSR form and agency review posture mean that transaction planning is getting more front-loaded, not less. The future Dealmaker will therefore win by mastering earlier regulatory mapping, cleaner data rooms, and better remedy planning, not by assuming that “market practice” will override enforcement attention.

The third trend is AI-assisted workflow. ESMA’s 2026 evidence-gathering on AI adoption in securities markets and the FCA’s AI Lab make clear that regulators expect meaningful deployment, but also governance. For Dealmakers, this means AI will increasingly summarize diligence findings, extract covenant changes across markups, map comparable transactions, and draft first-pass materials. But the center of gravity of the role will not disappear; it will move. Judgment, escalation, communication, and accountability will become more valuable because low-level synthesis will be cheaper. The great risk is that teams outsource thinking while retaining legal liability.

The fourth trend is a stronger linkage between product design, conduct, and post-close supervision. That is already visible in structured products, securitization, and public-offering disclosure. ESMA and the FCA emphasize target-market and product-governance analysis; SEC speeches and enforcement in structured notes emphasize pricing and valuation disclosure; and ABS reporting rules make post-closing transparency a continuing obligation. The future Dealmaker, accordingly, is less a one-time closer than a lifecycle risk manager whose work begins before launch and is tested after issuance.

The enduring conclusion is simple. The real Dealmaker in securities is not the person who merely finds a counterparty or secures a mandate. It is the person who can identify an opportunity, choose the right legal and financial path, build a diligence and disclosure process that survives scrutiny, negotiate the economic and documentary package without losing certainty, and then remain accountable for what happens after the press release. That is why the role remains hard to automate, easy to misunderstand, and central to capital formation.