Problematico:

It is often difficult to raise the budget of an IPO (Initial Public Offering). Moreover, there is a widely held wrong belief that an IPO is only possible after a company has validated its business model, has “traction”, has an order book.

Soluzione

As discussed in my previous article“Is your company ready for an I.P.O. Initial Public Offering ?”, the main barriers preventing an IPO to happen for a company which is ready, willing and able to pursue it are the following:

- Il costo di preparazione di un'IPO è proibitivo.

- Non vi è alcuna garanzia che l'IPO avrà successo.

- I banchieri e altri professionisti che mettono in gioco la loro carriera non autorizzeranno l'IPO senza:

- Adeguata due diligence che garantisca la sicurezza dei mercati mobiliari finanziari;

- Validazione del modello di business;

- Entrate sufficienti che rendano l'azienda almeno un flusso di cassa positivo e se non redditizio;

- Crescita forte e stabile.

In altre parole, non ci devono essere dubbi sul fatto che l'azienda sia sulla strada del successo.

I saw a number of companies with a high profitability potential that deserved investment banking services but could not afford them due to costs prior to the distribution of the securities, especially pertaining to the preparation and drafting of disclosure.

The Theory of Wagons

Secondo il mio mentore, poiché non ho trovato alcuna fonte di informazioni al riguardo, Howard Hughes ha inventato la teoria dei vagoni. Seguendo la leggenda, aveva installato un treno gigante nel suo giardino e dovette mettere più di un vagone per far viaggiare attraverso la sua proprietà gruppi di suoi ospiti. Vedere i carri attaccati l'uno all'altro lo ha ispirato a creare una teoria della crescita aziendale.

Pensava che la locomotiva, che è l'elemento più pesante del treno, simboleggiasse la sua azienda principale che era un'istituzione molto consolidata. Più un'azienda è ben radicata, più è vicina alla locomotiva e meno un'azienda è ben radicata, più è lontana dalla locomotiva. Le start-up sono nella parte posteriore del treno.

Usando questo modello, Howard Hughes utilizzava il flusso di cassa delle sue aziende con le migliori prestazioni per finanziare le sue nuove iniziative. Facendo un'analisi matematica finanziaria di base, sembra ovvio che tale sistema possa funzionare solo se le società di locomotive e primi vagoni sono altamente redditizie e che gli investimenti in nuove imprese sono di gran lunga inferiori a questa redditività. Secondo il mio mentore, un rapporto di 3 tra la somma delle aziende redditizie e l'investimento totale richiesto dalle start-up dovrebbe essere considerato un minimo per la sicurezza, ma non sono mai riuscito a capire come sia arrivato a tale rapporto.

Questa teoria mi ha fatto una grande impressione perché ho visto in essa un finanziamento a catena aziendale e ho pensato che potesse essere la soluzione per superare la prima barriera affinché avvenisse una IPO. Per molto tempo, mi sono chiesto come avrei potuto fare a cascata le IPO, la precedente tirando la successiva.

Quando sono venuto a conoscenza del JOBS Act (Jumpstart Our Business Startups Act), mi sono reso conto che il costo delle piccole IPO era stato drasticamente ridotto e quindi che ora era possibile finanziare le IPO attraverso un processo a cascata di domino.

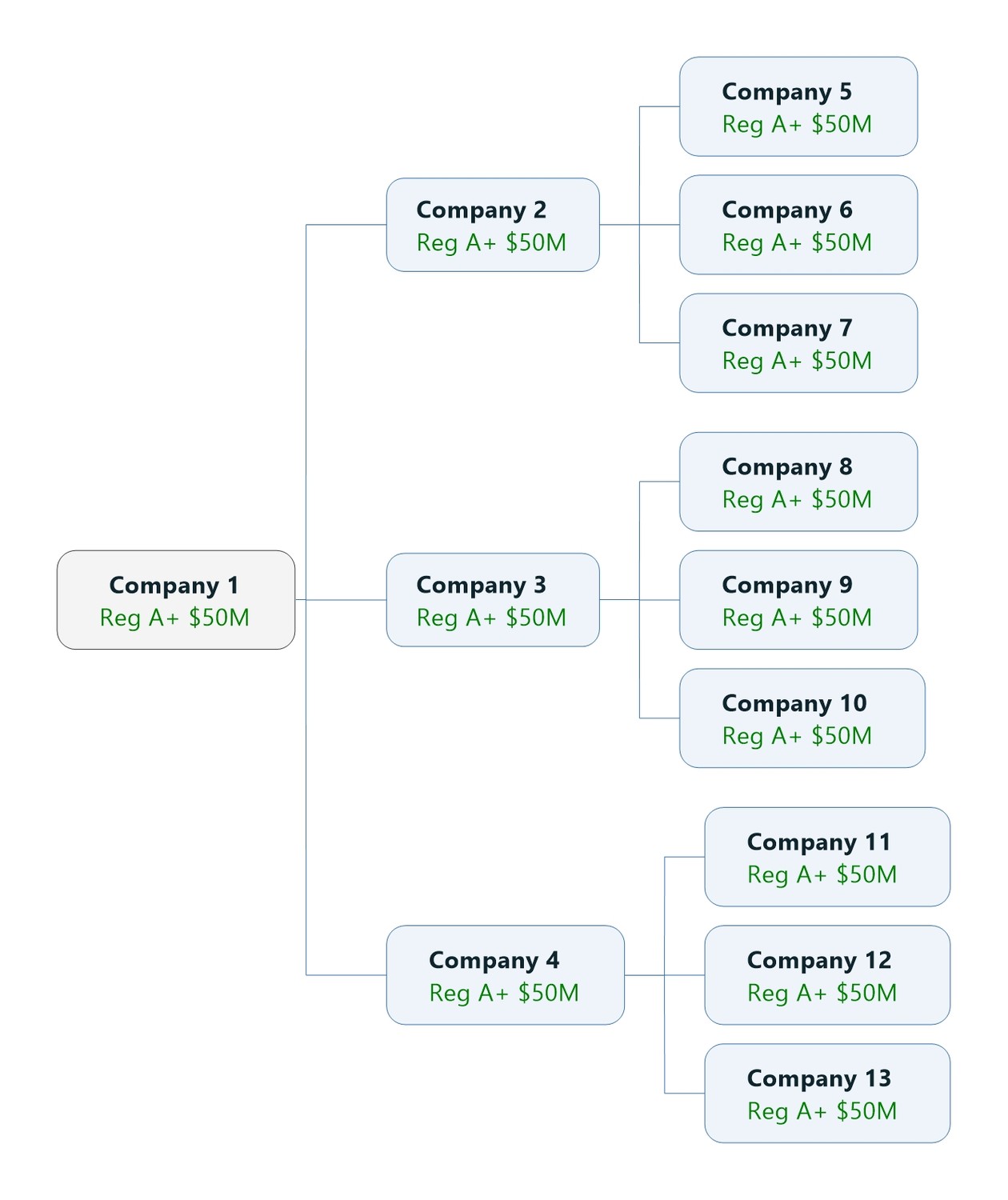

La mia prima idea è stata quella di prendere una parte dei proventi della prima IPO per finanziare altre tre IPO e applicare lo stesso principio a dette altre tre IPO come nello schema qui sotto.

Tuttavia, c'erano una serie di problemi dal punto di vista della regolamentazione dei mercati mobiliari e dal punto di vista della divulgazione.

How to avoid these IPOs to be considered a group of companies acting in concert by the regulator ?

Simply by concluding an IPO Development Agreement between an IPO Incubator and the future Issuer for the financing of its IPO.

How to avoid the birth of a tree of shareholding relationships among all these companies ?

Simply by concluding excluding from this IPO Development Agreement between the IPO Incubator and the future Issuer any purchase of shares of stock.

Preliminary Financing of the Incubator

- USD 2 million are raised in the Incubator through either a loan or an equity investment.

- The Incubator goes public and raises USD 50 million through a Regulation A+ Tier 2 registered offering of shares of common stock.

- If the Incubator was financed through a loan, the Incubator will reimburse this loan with interest and pay a Premium Bonus to its creditor/s.

Procedure & Sequence of Events for an IPO Candidate

- The Incubator enters into a Development Agreement with an IPO candidate company, in other words a potential securities issuer willing to distribute its securities to the general public to raise money.

- This Development Agreement provides that against the financing of the IPO candidate’s Regulation A+ registered offering for a maximum of USD 2 million, the IPO candidate shall immediately remit 20% of its issued and outstanding shares of stock, and that upon successful IPO, shall pay Incubator 12% of the proceeds.

- The IPO candidate proceeds with its IPO and thus becomes a public securities Issuer and public company listed on the NASDAQ or the New York Stock Exchange. Moreover it is funded with USD 50 million.

- From the IPO proceeds the Issuer (ex-IPO Candidate) pays Incubator 12% of the proceeds.

- So, in case of a typical Regulation A+ Tier 2 registered offering of shares of common stock raising USD 50 million, the Issuer will effectively pay to the Incubator USD 6 million.

Structure of Cascade depends on the Type of IPO

- The Incubator can finance between 1 and 24 Reg A+. We will call this number n the number of parallel processes. On the left figure, n = 3.

- If the Incubator has USD 50 million and wants to finance small S-1 IPOs, n will be reduced to 10.

- If the Incubator has USD 50 million and wants to finance large S-1 IPOs, n will be reduced to 5.

Sequence of Events for the Cascade of IPOs

- The Incubator enters into a Total of T Development Agreements (described under §4 and §5 hereabove) with n IPO candidate companies, in other words n potential securities issuers willing to distribute its securities to the general public to raise money.

- The IPO candidates proceed with their IPOs and thus become public securities Issuers and public companies listed on the NASDAQ or the New York Stock Exchange. Moreover they are funded with USD 50 million at least, depending on the type of IPOs.

- The Incubator receives:

- ts commission on the funds raised in the IPOs according to the the formula: 12% . IPOraise(T). On a cluster identical to the left figure with n = 3 there are 13 companies. Assuming they all do USD 50 million raises with USD 6 million commission for the Incubator, the Incubator shall receive USD 78 million in cash.

- 20% of the issued and outstanding shares of stock of each candidate. The amount represented cannot be quantified as it depends on each corporate valuation.