Page 104 - Initial Public Offering - An Introduction to IPO on Wall Street

P. 104

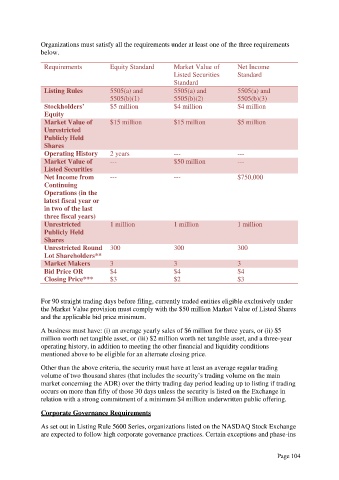

Organizations must satisfy all the requirements under at least one of the three requirements

below.

Requirements Equity Standard Market Value of Net Income

Listed Securities Standard

Standard

Listing Rules 5505(a) and 5505(a) and 5505(a) and

5505(b)(1) 5505(b)(2) 5505(b)(3)

Stockholders’ $5 million $4 million $4 million

Equity

Market Value of $15 million $15 million $5 million

Unrestricted

Publicly Held

Shares

Operating History 2 years --- ---

Market Value of --- $50 million ---

Listed Securities

Net Income from --- --- $750,000

Continuing

Operations (in the

latest fiscal year or

in two of the last

three fiscal years)

Unrestricted 1 million 1 million 1 million

Publicly Held

Shares

Unrestricted Round 300 300 300

Lot Shareholders**

Market Makers 3 3 3

Bid Price OR $4 $4 $4

Closing Price*** $3 $2 $3

For 90 straight trading days before filing, currently traded entities eligible exclusively under

the Market Value provision must comply with the $50 million Market Value of Listed Shares

and the applicable bid price minimum.

A business must have: (i) an average yearly sales of $6 million for three years, or (ii) $5

million worth net tangible asset, or (iii) $2 million worth net tangible asset, and a three-year

operating history, in addition to meeting the other financial and liquidity conditions

mentioned above to be eligible for an alternate closing price.

Other than the above criteria, the security must have at least an average regular trading

volume of two thousand shares (that includes the security’s trading volume on the main

market concerning the ADR) over the thirty trading day period leading up to listing if trading

occurs on more than fifty of those 30 days unless the security is listed on the Exchange in

relation with a strong commitment of a minimum $4 million underwritten public offering.

Corporate Governance Requirements

As set out in Listing Rule 5600 Series, organizations listed on the NASDAQ Stock Exchange

are expected to follow high corporate governance practices. Certain exceptions and phase-ins

Page 104